Searching For Multibaggers

Searching For Multibaggers

Intellicheck Inc. (IDN)

Welcome to Beating the Odds. Our goal is to create and curate content on investing, strategy, tech, fashion and anything else we find interesting.

Watching a stock you used to own go on to become a multibagger hurts, but it’s part of the game.

Square (ticker: SQ) and AMD (ticker: AMD) are a couple of stocks I had this unfortunate but necessary experience with.

SQ

I sold at $25.10 in August 2017 and finally re-entered in the summer of 2020.

AMD

I sold at $12.98 in August 2017 and ended up missing a 7x run.

ETH

I’ve actively managed a portion of my portfolio since early 2017 and my first big multibagger was actually in crypto (lol). I was lucky enough to pick up a slug of ether (ETH) in the $12 - 50ish range starting in February 2017.

I didn’t sell at the very top but made out with a healthy profit selling in chunks along the way. What a ride.

I’m always on the lookout for potential home runs to place smallish bets on and recently came across a few intriguing setups. Here’s to hoping this is the next bagger.

Intellicheck Inc. (ticker: IDN)

Key Metrics (data as of 1/4/21 market close from Koyfin):

Market cap: $214.66M

Stock price: $11.66

Trailing twelve months (TTM) revenue: $10.55M

NTM (Next Twelve Months) revenue analyst estimate: $14.77M

Enterprise Value / NTM revenue multiple: 13.7x

YoY rev growth as of Q3’20: +40% ($2.699M vs $1.93M million for the same period last year)

Gross margin (GM): 89.1%

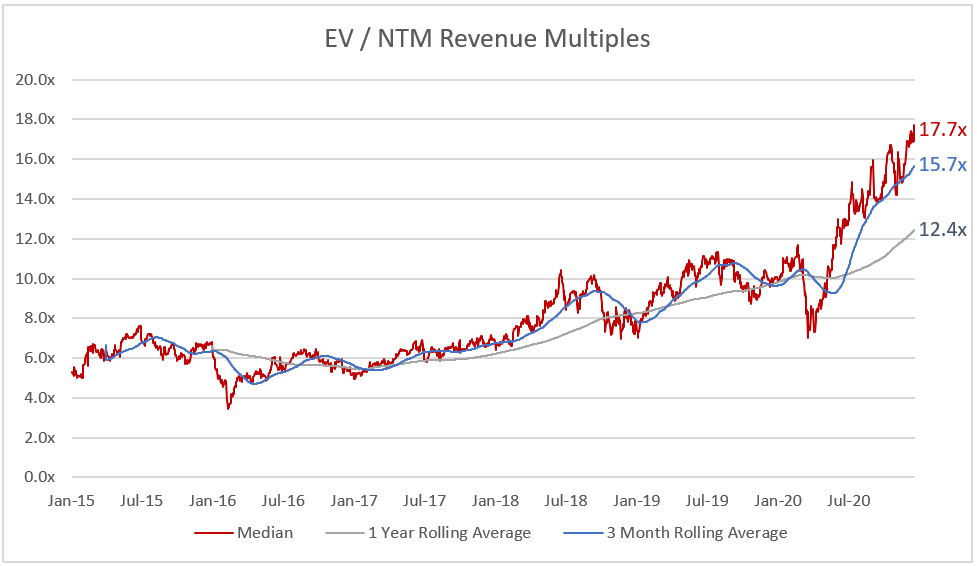

For context, here’s the current state of Enterprise Value / NTM revenue multiples for SaaS companies tracked by Jamin Ball at Clouded Judgement (as of Q3 earnings):

How many SaaS companies can you think of that fit this profile: 40-100% YoY revenue growth, virtually no competition, almost 100% retention rate, and trades below the median EV /NTM Rev multiple?

Intellicheck is the industry leader in real-time identity authentication and validation solutions. Their patented ID Document Authentication, Optical Character Recognition (OCR), and Facial Recognition capabilities quickly and effectively verify identities. Currently, their portfolio includes 20 patents related to identification technology and other similar areas.

IDN’s solutions make it possible for those in Financial Services, Retail, Age Restricted Products, Law Enforcement—anywhere authentication is required in both in-person and person-not-present environments—to instantly and accurately authenticate an individual’s identification.

IDN primarily sells its software to the issuers behind private label credit card programs. 12 companies (ten banks plus Amex and Discover) are responsible for 99% of these programs. The banks then push the software to their retail partners (since the banks eat the cost of the fraud).

Taking a look at the stock chart, IDN is a classic turnaround story that recently hit an inflection point.

IDN’s Board appointed Bryan Lewis as CEO in February 2018. In Q2 2018, IDN pivoted from per store to per scan pricing and focused on selling to banks, not retailers. They also adjusted their approach to selling solutions by use cases instead of as a singular packaged product—this presented better upsell and cross-sell opportunities.

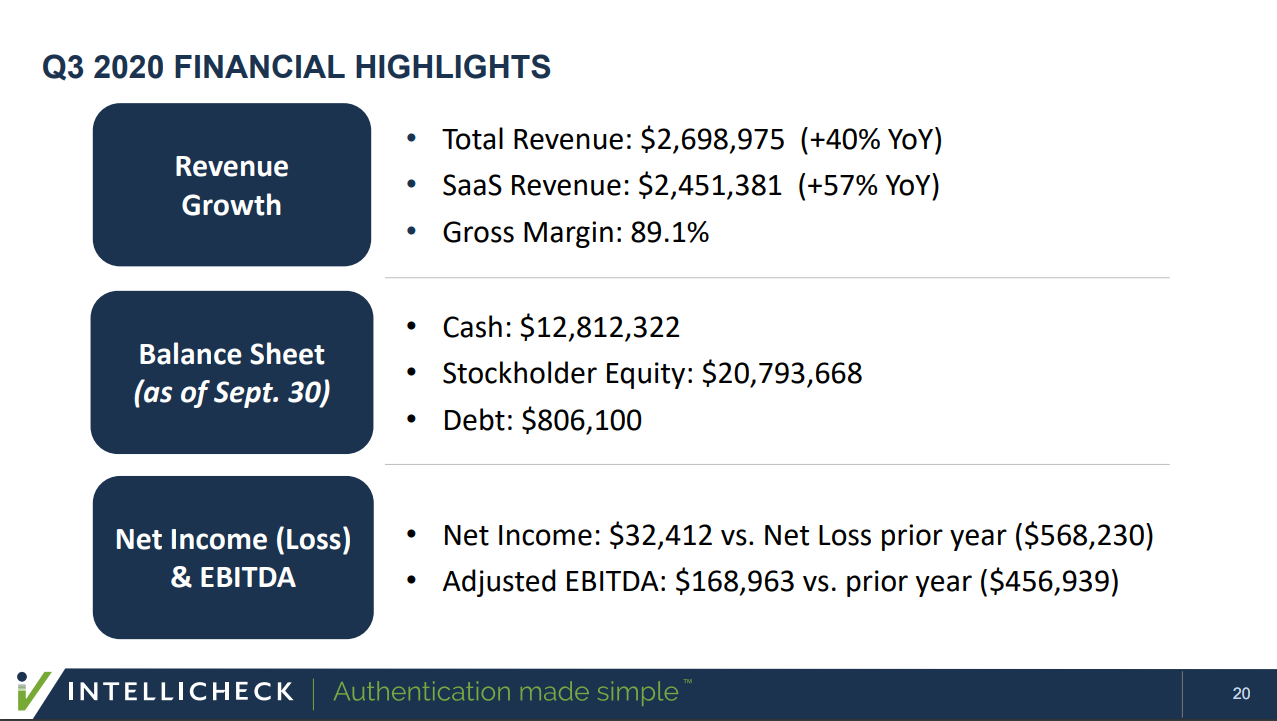

Q3 Highlights

From IDN’s Q3 earnings presentation:

Additional financial highlights:

YoY SaaS revenue growth over last 6 quarters (starting Q2’19): 79%, 140%, 210%, 160%, 49%, 57%

Adj. EBITDA positive since Q4’19 (except for Q2’20 due to negative COVID impact)

~85% GM is sustainable going forward

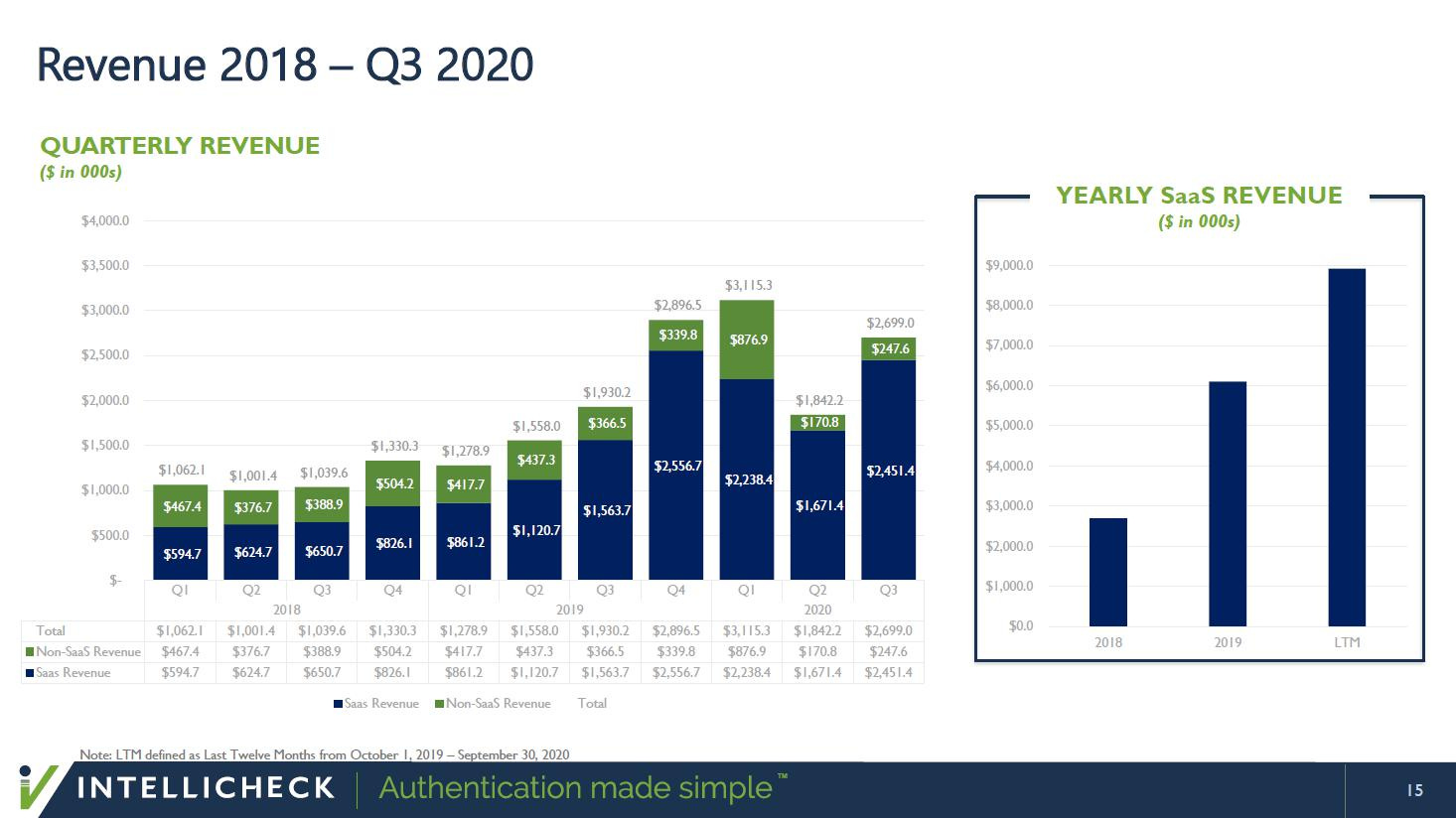

Revenue growth visualized:

Major growth drivers: turbocharging sales & marketing is a top priority for management, price increases, secular growth of authentication use cases

IDN was recently recognized by Gartner in the Gartner Market Guide for Identity Proofing and Affirmation. The annual guide is a resource for decision-makers across industries who are charged with safeguarding their organizations and clients from incidents of identity theft and fraud.

According to Gartner, “By 2022, 80% of organizations will be using document-centric identity proofing as part of their onboarding workflows, which is an increase from approximately 30% today.”

Now let’s hear directly from company management

5-minute interview with CEO Bryan Lewis provides a quick overview of the company—dated June 2019:

Here’s a video from June 2020. Some good info on how the business adjusted during the pandemic, tailwinds, etc.

The most comprehensive and best watch in my opinion. Dated 11/24/20, a presentation from the CEO and CFO Bill White. This discussion includes company strategy and moat, competitive analysis, financial highlights, and a mini product demo, among other things. Good summary in this thread.

Risks

Economic slowdown or COVID restrictions negatively impact the per-scan revenue model (the revenue recovery from Q2’20 to Q3’20 is encouraging given the backdrop of COVID-19)

Sales & marketing strategy doesn’t live up to the hype

IDN accepts a lowball buyout offer (management has hinted at a buyout as the ultimate goal for the company)

Company technology becomes obsolete or inferior to competitors’

Conclusion

It might just be the auditor in me, but I’m really high on Intellicheck’s prospects. Overall, I believe company management is competent and laser-focused on growth, the risks are low probability and manageable, the market opportunity is attractive, and the valuation is reasonable. Long IDN.

Further reading:

Informative Twitter threads (sorted by date): here, here, and here

Start with the early 2018 conference call transcripts, when Bryan Lewis become CEO, to see how he transformed the business

Earnings report presentations (8-K Forms)

Excellent IDN investment thesis from Max Capital

Thanks for reading! As always, questions, comments and feedback are appreciated. Subscribe below to be notified of future posts.

Disclosure: None of this is investment advice. I own ETH, SQ and IDN shares.